The first thing to know about tokenisation is that it is not new.

Around 1564, some bright spark in Italy thought, “Why don’t we issue tokens to our depositors, and then let them use those tokens to trade, rather than having to manually withdraw their silver every time they want to do something interesting?”. So that is what they did¹.

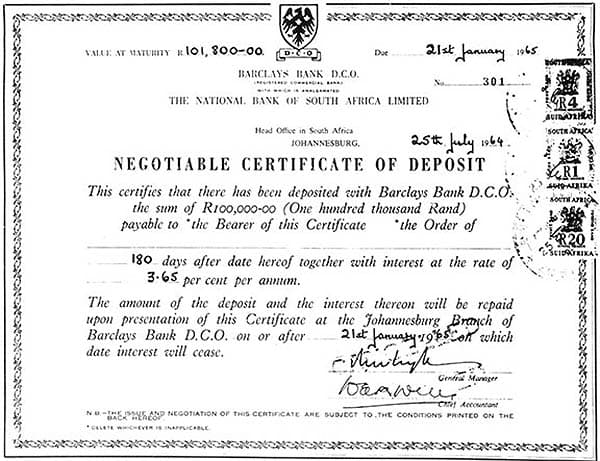

A more recent version, the negotiable certificate of deposit (NCD), was made in February 1961 by the First National City Bank of New York. These NCDs, along with Repurchase Agreements (repos) and Government Treasury bills (t-bills), are what constitute the modern “money market”.

One of the first NCDs of this kind was issued 3 years later by Barclays, in South Africa, denominated in Rands. This was also 3 years after the Rand became a thing (side note: it has since lost more than 99% of its domestic purchasing power, and it is arguably the best-performing currency in Africa).

All these instruments are already tokenized, the people who made them just didn’t use that term. So, when we talk about tokenisation, we’re not talking about something new: we’re debating the medium in which various assets are created and traded.

The Obvious Stuff

So, let’s begin with the advantages a public, programmable ledger has as a medium for creating and trading assets.

- Atomic Delivery vs. Payment (DvP) without a central counterparty (CCP)

- No settlement risk

- Lower fees

- (Potentially) more liquid secondary markets

That’s it. At the risk of missing some nuance, everyone who sells you something more than the above is probably a snake oil salesman.

These features are important, though! They really do change the game in many ways.

Consider repos. If your agreement is onchain, and the collateral is too, then there is verifiable and unequivocal possession. When repayment occurs, transfer happens simultaneously, guaranteed by code running on a public machine shared by everyone and owned by no-one. That is very cool. It would have impressed the Italians. The fact that the agreement is code that can itself be traded securely and transparently is the recursive cherry on top.

Given that delivery and payment are atomic–they occur at the same time, in the same transaction and one cannot happen without the other–there is no settlement risk². There is also no need for brokers, fidelity insurance or many of the things which contribute to higher fees when trading these assets.

Accessibility Traps

The term “access” is meaningful when we’re talking about assets that don’t have liquid markets. Tokenization can help create those markets, and so make the primary market more efficient.

You can tokenize local municipality bonds, and sell those tokens to global investors. This might bring more liquidity into an illiquid market, which compresses the spread in the primary market. It might make municipal bonds behave more like national ones³.

This is what NCDs did for large depositors. History is proof that creating liquid markets where none previously existed is a super power. If I don’t need to rely on the issuing bank, but can find someone to buy my NCD on the open market–where its price is continuously discovered–that is a net positive because the whole system becomes more resilient and manipulation-resistant. The market allows the depositor to get out before maturity, albeit at an un-guaranteed price, while the bank can hang on to the money until maturity.

By the same token, “access” is not meaningful for already-liquid money market funds; or high volume, low margin bond markets; or most government t-bills. For already-deep markets, "access" is a cost, not an advantage, because meeting retail's shorter-term liquidity demands dilutes the underlying yield⁴.

To put it differently: when accessibility is sold as some kind of moral good (because we’re opening markets to people previously barred from them) or as marketing ploy (because it makes us look innovative) then there will likely be an inverse correlation between the extent of that “accessibility” and the returns any instrument can deliver.

“Accessibility” is not always about morals or marketing, it can just be about creating FOMO. BlackRock might try to sell you with “access” to stuff you couldn’t previously trade, but they will charge you for the privilege. The Bitcoin ETF is their most profitable ever, and it is built upon an asset the premise of which is self-custody and peer-to-peer transacting. The irony is palpable.

“Access” must indicate how and what kind of liquidity can find its way into a market, as that is what determines how efficiently prices are discovered. If it means something else you are–again–being sold snake oil, even (perhaps especially!) when it is Larry Fink pitching you.

More Permissions, More Problems

We’re interested in tokenizing assets in ways which alter the architecture of power. By this, we mean: do not add permissions intended to mimic how things work in the “real world”. It limits the amount and kind of liquidity that can enter a market. If power is still a function of who can get in and out, rather than what they contribute to price discovery, nothing has changed and the markets that emerge will be no better.

ERC 3643 demonstrates the irony effectively: a permissioned standard in an environment that is fundamentally pseudonymous and open to all. It is like putting a few gates on the beach to try and stop people from getting into the ocean.

CIP 56 illustrates the irony in a different way. Canton is built to be restrictive, controlled by corporations, and customised to institutional needs. Canton is where most “Real-World Assets” (RWAs) are currently listed, but you cannot trade there yourself in almost all cases, and no-one can see what is going on, by design (corporations will try to convince you they require privacy). There might be more liquidity in Canton markets, but it is of a specific, institutional kind. Liquidity cannot easily enter and participate in price discovery outside of that already controlled by the permissioned members of the cartel⁵.

The Actual Hype

Our thesis is that accessibility–meaning, very specifically, how much and what kind of liquidity can enter a market–is the single most important measure of the long-term value of any token⁶.

The question that really matters is, “Does this token create a liquid market where once there was none?”

The most liquid markets are not created by trading underlying assets themselves; they’re created with perpetual swaps. There is already such scale in these markets that perps are discovering the prices that Bloomberg quotes over weekends for commodities like oil or silver, or indices like the S&P 500.

These markets attract more–and more diverse kinds–of liquidity and so are more efficient and resilient. If you don’t believe that, then remember that derivatives (tokenized or not) are naturally more suited to most trading, especially when the underlying is a security that, when traded directly, is subject to securities transfer taxes, brokerages, and settlement guarantee levies⁷.

Derivative tokenization is well under way. It doesn’t depend on jurisdiction. It doesn’t draw arbitrary lines between what is “real” and what isn’t, or between “developed” and “emerging” markets. It doesn’t require permission to participate. It attracts all kinds of liquidity, from all sorts of different actors. It doesn’t care if you are an individual, a fridge, or Jane Street Capital⁸.

It is the kind of innovation that justifies moving what we have been doing for 500 years into a new medium, because that medium has properties which enable us to create and trade assets in fundamentally more accessible, and therefore efficient, ways.

Principled Derivatives

How does this apply to the markets in which LAVA operates?

How can we apply HIP-3 and HIP-4 in ways that provide global, liquid markets with access to African opportunities?

Because access–in our terms–is a two way street, this also means “in ways which give Africans access to global liquidity” such that they can discover their own prices more efficiently, directly, and transparently than they otherwise could.

It doesn’t have to be Hyperliquid specifically: it is the principle of leveraging global primitives that are genuinely accessible (and therefore deeply liquid) which we are pointing at.

The forms we see this taking include, but are not limited to:

1. Permissionless Price Discovery

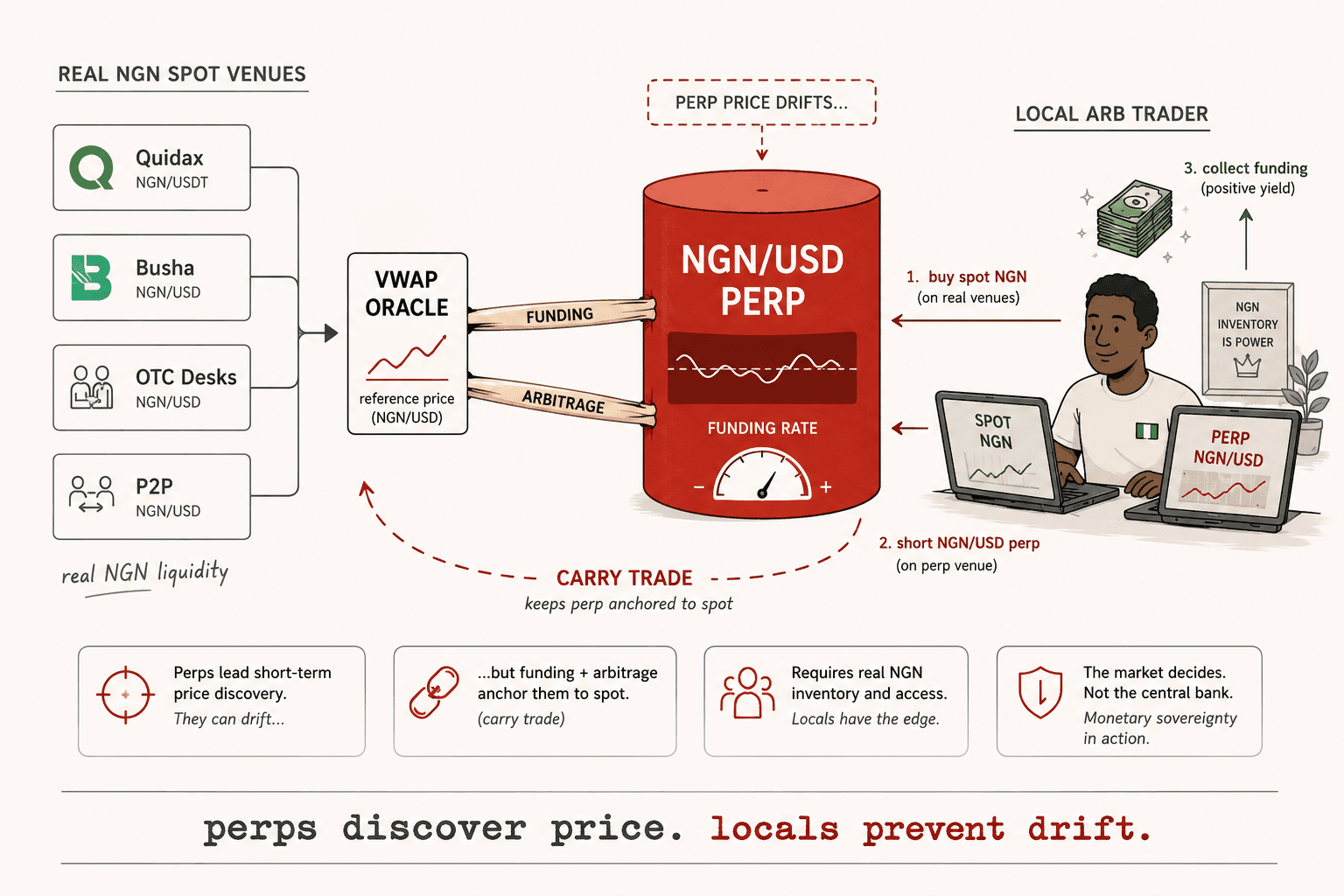

It is possible to build more reliable means of discovering the price of local currencies in a way that cannot be manipulated by the central banks⁹. How? A perpetual swap on the currency. Perps lead short-term price discovery, but they can’t drift freely because funding and arbitrage keep them anchored to spot. So, for this to actually work, we need a reliable spot price (the exact problem we’re trying to solve!).

It is possible to build good oracles from diverse venues in emerging markets. Our portcos do it all the time. We’ll be open sourcing some code that does this for the Naira in the near future. A reliable oracle is only half the problem, though. The mark price can be set by this oracle, but you still need people to arb the difference between perp and spot to bring them back in line (generally called a “carry trade”).

The key point is that we need inventory on venues with actual Naira in order to perform such carry trades. Therefore, only locals with access to such accounts can fulfill this role. Which is curious, because it means that the monetary sovereignty we’ve talked about when analyzing local stablecoins might shift from governments and regulators to people actually using the currency in ways which create value. Wouldn’t that be one for the books?

2. Open Financial Infrastructure

Maybe you think that sounds too fantastic. Maybe you think the 500,000 HYPE you need to stake on venues like Hyperliquid to open your own perp market makes it practically infeasible. Use HIP-4 and binary options instead! HIP-4 enables more than just prediction markets.

To keep it simple at first, we can create a binary option for, “Will the Naira close the day (in Nigerian markets) at or above 1380 to USD?” The market resolves at 17h00 WAT every weekday, and it resolves to either 0 or 1 depending on the official price (or depending on whichever oracle you choose if you want to have a more realistic option).

There are no margin requirements and no liquidations. Just tokenized exposure to the price of the Naira without any intermediaries, and with significantly lower fees than anywhere else in the world. That’s just the beginning.

What about binary options that let people get synthetic exposure to any stocks without having to go through a broker and pay exorbitant fees (common in Africa), and without having to ask for permission or maintain margin? Or, leverage Dean’s ideas to build credit default swaps, reinsurance, catastrophe bonds, weather derivatives and so on¹⁰.

Even deeper than that: the introduction of expiry as a first class object in HyperCore via HIP-4 makes it possible to program zero coupon bonds (ZCBs). Most financial instruments can be decomposed into some combination of ZCBs¹¹. So, this is really about how, with surprisingly few primitives, you can actually bring “all of finance” onchain.

The space for people building the Trade[XYZ] of ZCBs is wide open, and the potential market for this, when they are composed in intelligent ways, is even bigger.

3. Transparent Options

Maybe you don’t like Hyperliquid at all, and disagree that perps are likely to be the dominant form of derivative due to the depth of liquidity they attract and the ease of trading they enable. There are options that can’t currently be created using the primitives we have discussed above. Such instruments can, for example, provide transparently-priced ways to hedge FX risk with very little working capital (a key need for many African businesses).

Read our research on this here.

4. What Doesn’t Apply

The shared theme underpinning all the above is making advanced financial tools accessible to people who live close to idiosyncratic problems, because they are best-placed to solve them.

The form we do not think tokenization takes long term is having to KYC to buy exposure to “real” assets like grain or real estate, where the venues you can trade it are restricted, and the underlying is easy for a cartel to manipulate, precisely because they maintain a monopoly on what counts as “real” and what doesn’t.

The bright sparks we’re looking for won’t shoehorn old ownership models into digital infrastructure and inherit all the same trust problems. They may care about private credit, though private credit is both having a moment and melting down in the US right now. Tokenizing private credit may just lead to more redemption requests and behaviour akin to bank runs.

There will be markets for what others call “ownership” and “issuer liabilities”, but they will not be as big, or efficient, as derivatives. This is because of deep architectural tensions: tokenizing ownership or private credit means agreeing to play by someone else’s definition of “real” and so re-introducing custodian risk, the need for insurance, brokers, auditors, jurisdiction by jurisdiction licenses, and permissions around who can and cannot participate.

The net result of which is that liquidity remains fragmented and the market doesn’t achieve the critical mass required to become a genuinely effective and resilient means of price discovery for whatever is being traded.

We see a lot of teams trying to do some version of the above in Africa: corporate paper, fixed deposits, tokenized MMFs, etc. There are some interesting insights in each one of these. However, these teams need large amounts of capital to either secure the relevant licenses or to meet the capital requirements for those licenses.

Sponsoring jurisdiction-specific licenses is unlikely to lead to the highest ROI for a fund focused on how Africans can leverage global tools to build the future of finance on the continent.

We’re looking for the bright sparks who can see beyond the current landscape and what we are told we need to do to fit in.

Power Without Permission

Despite what you may read, tokenization is not about entrenching institutional power: it is about creating better alternatives. It is about genuinely open access to resilient markets that are not controlled by extractive cartels. It is not about who you are, or where you live. It is about how we can all discover the prices for increasingly diverse things without anyone sitting between us.

The way to that world is not through permissioned token standards, regulations, and jurisdiction-specific licenses. The way will not be walked by people who are just being pragmatic. Hyperliquid has no licenses, a team of 11, and $300T traded there in 2025.

Everything revolves around liquidity. How much can access the market? Is it limited to “only accredited investors” or “only KYC’d participants” or “only institutions”; or can anyone join? These are the questions that will define the investments we make in this world.

We’re excited to participate in creating and trading assets on public, permissionless ledgers, with a specific focus on making them accessible, such that markets the world over become more efficient.

There is a singular opportunity before us to invest in open financial infrastructure that builds trust precisely by removing permission and those who would or would not grant it. We intend to grab that opportunity with both hands.

Notes

¹ Except, obviously, he thought this in Italian and called the tokens fede di deposito, but you get the point.

² There is some nuance here around both smart contract risk (which we think is distinct) and certain cases where mechanisms like ADL cause “socialized losses”. These are not losses in the traditional sense, because they apply in extremely volatile conditions where trades are automatically closed out, limiting profit, as opposed to taking away any principal. Read more here.

³ Or you could tokenize certain debt notes such that the people who buy them are not locked in until maturity, but we will have more to say about private credit, or issuer liabilities, later.

⁴ ETFs already avoid this problem by enabling their tokens to trade on a secondary market.

⁵ Consequently, the most accurate financial statement of where Canton revenue comes from is currently here. Contrast this with the financial reporting that is possible for a network like Hyperliquid, and the amount of data that is consistently available.

⁶ “Value” here is not equivalent to “price”. Accessibility may not make the price of the token moon, but it will make the token a valuable representation in that it can be used–by virtue of the medium in which it exists–to make the market more efficient, more transparent, and more liquid. Its value is more about the utility it provides rather than the relative measure you can accumulate by holding it.

⁷ Some analysts already show how the “Readiness” table of the “$400T Future of Tokenized Assets” report written by Keyrock and Securitize is inversely correlated with the assets that are actually being tokenized, because it’s not about standardization or regulatory clarity: it’s about liquidity.

⁸ It is worth noting that, in this, we are diametrically opposed to a16z, who say, “Instead of being a derivative, it’s the real thing.” We think that “The guardrails the largest institutions needed are already on the horizon” is exactly the kind of phrase that illustrates why markets created with and through such intermediaries will never be as efficient as their perpetually open cousins.

⁹ Perhaps you believe central banks “set” the price, rather than manipulate it, and that this could potentially be a good thing for emerging markets under pressure from dollarisation and other forces outside their control. Whichever word you choose, the point is that–crypto maximalist or not–central banks are systematically incapable of fulfilling their mandates. They are–in the words of the creator of the modern framework for how they work, Walter Bagehot–a “moral hazard”.

¹⁰ The CDSes will be important as more people try to tokenize private credit: a point we are still getting to.

¹¹ Zero-coupon bonds (ZCBs) are the building blocks of finance because they represent a single, guaranteed cash flow at a specific future date. By combining ZCBs with different maturities (a "ladder") or by stripping interest payments from coupon bonds, any fixed-income instrument can be synthesized.