A stablecoin only becomes infrastructure when you can quote it tightly, move size through it, and trust that the price you see is the price you will get. Issuance is the easy part.

When the local stablecoin is not liquid, people choose the instrument that is. If cNGN is too shallow, Nigerians who need liquidity, inflation hedging, or a credible USD/NGN reference will route around it via USDT P2P and informal OTC channels.

As we have discussed previously, monetary sovereignty, capital controls, financial integrity, and data visibility matter. Foreign-stablecoin substitution can weaken domestic policy transmission and move activity away from regulated institutions. Both problems share a root: nobody will use a market they cannot trust, and nobody can supervise a market they cannot see.

The first article in this series argued that local market makers contribute to geographic decentralisation, and introduced some open source software to make that case more concretely. This article is the data: what the market for cNGN looks like today, and what it implies for the people who supervise it.

The Venues

We consider four venues to gather pricing data for cNGN:

- Quidax, a licensed CEX in Nigeria. The only venue where cNGN/USDT has an executable book today.

- Uniswap V4 pools on Base and BSC. Always-on, public, but very thin.

- Bybit P2P, a useful NGN/USD reference for where the street prices the Naira, and the highest volume place for p2p trading.

- Display-only venues like AssetChain and Blockradar, which show a price but are not venues we trade against.

These surfaces disagree with each other for structural reasons: bank hours, fragmented inventory, different user bases, gas, the novelty of cNGN as an asset, and the persistent divergence between bank rates and market rates in Nigeria. A market maker's job is to work out which disagreements are opportunities and which are noise.

The Centralised Limit Order Book

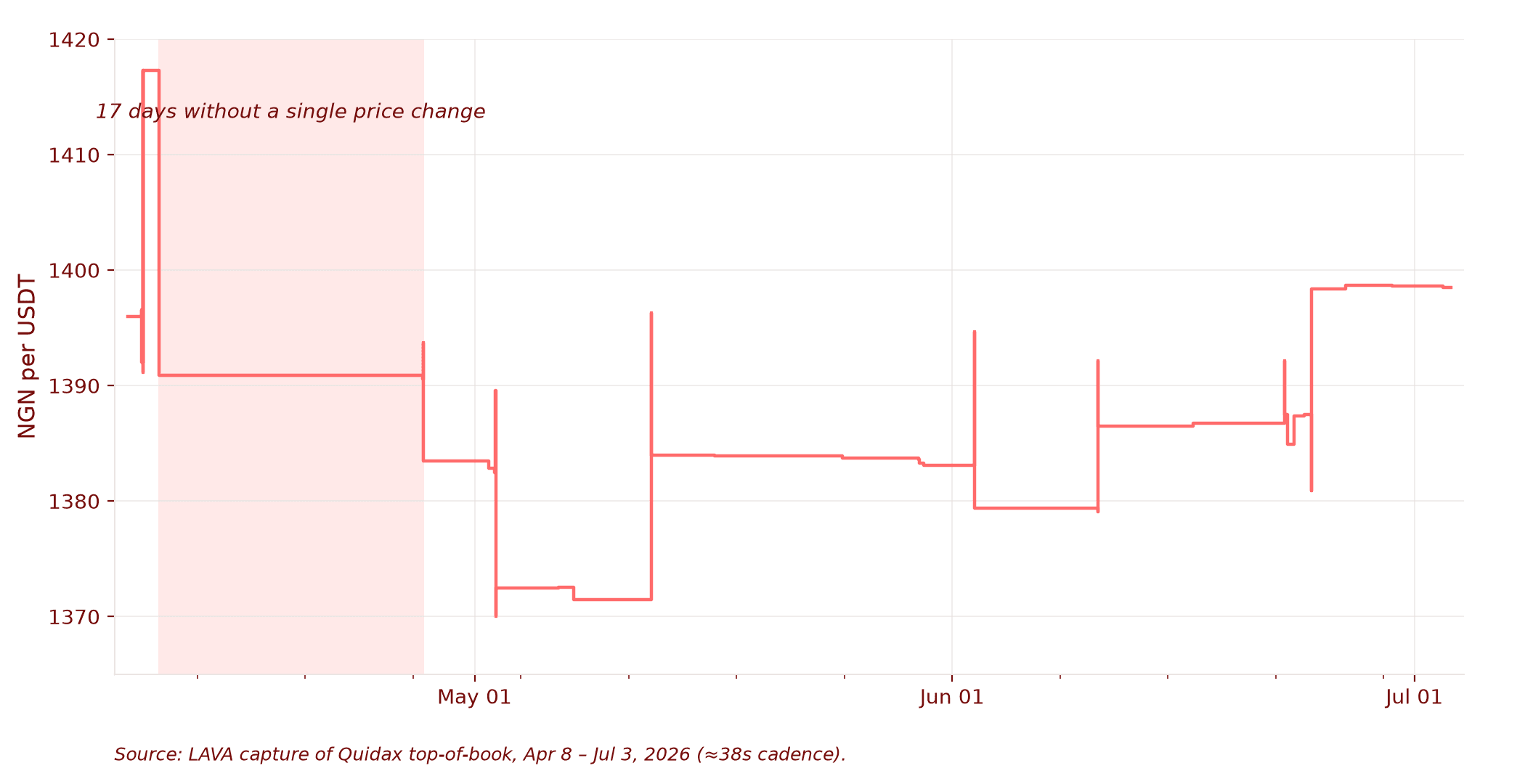

We captured the Quidax cNGN/USDT top of book every ~38 seconds from April 8 to July 3: 255,846 snapshots*.

At first glance the book looks healthy. The median spread is 33 bps. The spread is under 50 bps in 65% of snapshots and under 100 bps in 98%. For an exotic pair on a regional exchange, those are respectable numbers.

Then you look at how often the price moves.

The mid changed 95 times in 86 days, only changing on 21 distinct days. The longest stretch without a single change ran 17 days, from April 10 to April 27. Over the whole period the mid ranged from 1370 to 1417.

A liquid USD stablecoin pair moves its mid more in one minute than this book moved in three months.

Nobody is trading through the top of the Quidax book often enough to force it to update, which means the book is not discovering the price of the Naira.

What Stress Looks Like

The other thing the data shows is how this market behaves when quotes do actually move.

Eight times in the period, the spread stretched past 150 bps. The pattern is consistent: the tight ask disappears or jumps ~26 NGN higher, the mid lurches with it, and then the book heals. Half these episodes resolved inside 20 minutes; one lasted roughly a day. These are quote pulls, not trades: the mid snaps back to where it started, which real flow would not do.

Thirty-one of the 101 quote changes in our capture are the same move: the bid stepping up by 0.2 to 0.6 NGN, once per polling interval, with the ask untouched. That is one participant's ladder walking the bid back into place. However the spread recovers, it recovers one participant deep. In 297 snapshots there was no ask at all: for stretches of time, you could not buy cNGN on the only executable venue at any price.

None of this is a criticism of Quidax. It is what an early market looks like from the inside, and it is exactly the environment we said local market makers would be entering. Where quote recovery is one ladder deep, a second ladder doubles the market's resilience.

The DEX

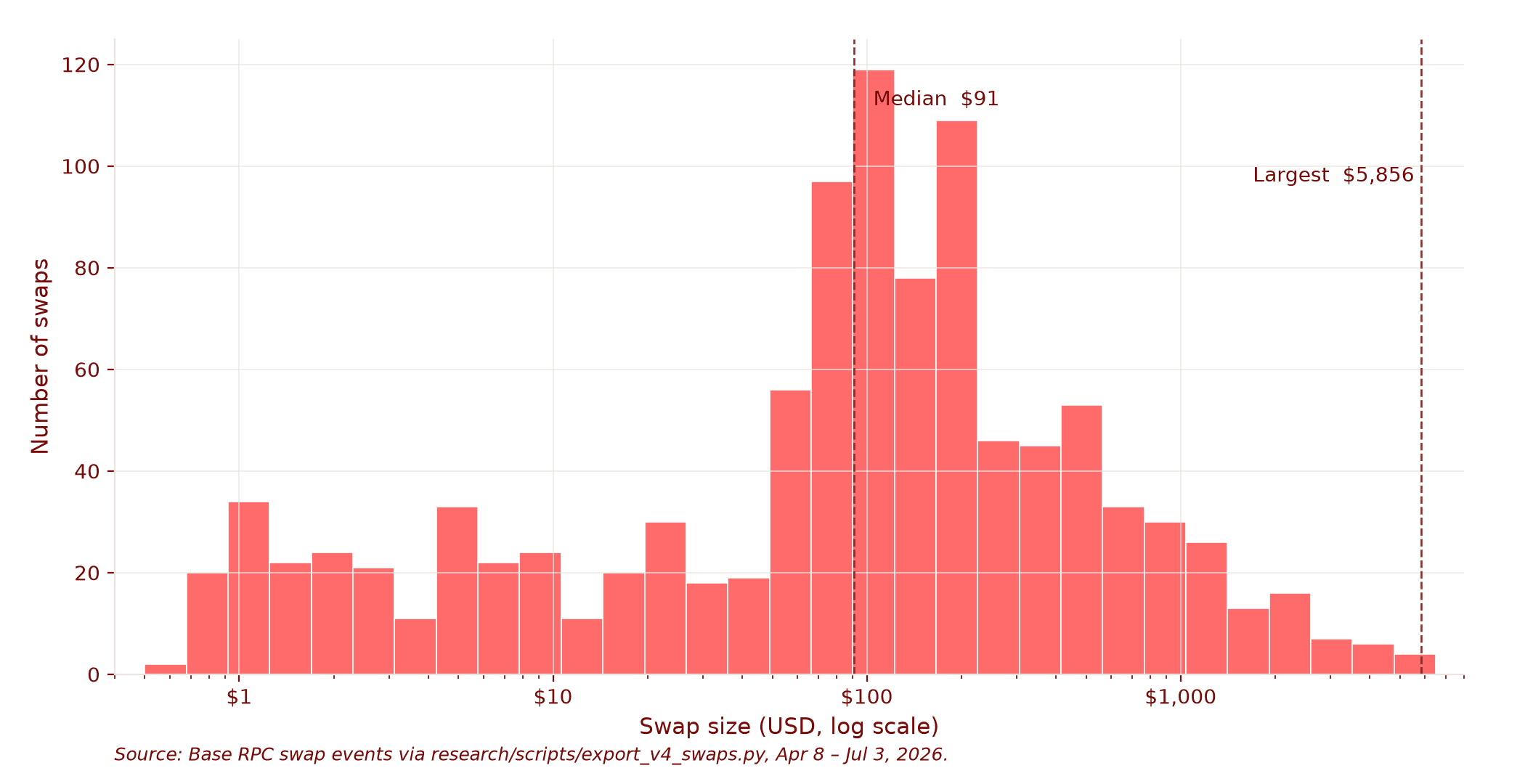

For the onchain markets, we can fetch the full swap history of the Uniswap V4 cNGN/USDC pool on Base (the larger of the two pools). Anyone can reproduce this data using our scripts.

Over the same 86-day window, the pool traded 1,160 times, on 84 of 86 days, with a median gap of eight minutes between swaps. Every swap prints a new price by design. What matters is that all these prices spanned roughly the same band: 1367 to 1410 Naira per dollar against Quidax's 1370 to 1417.

Those 1,160 swaps carried about $316,000 in total. The median swap was $91. The largest was $5,856. The pool discovers price continuously, in retail-sized increments, but could not absorb a single institutional ticket without moving through its whole quarterly range.

So, the two executable surfaces fail in opposite ways. The order book shows size but no movement: a price you can touch but should not believe. The pool shows movement but no size: a price you can believe but cannot touch for more than a few hundred dollars.

Neither alone is a market. Together, checked against each other, they might begin to behave like one, but both require more liquidity and more participation. This is thorny territory for regulators. Part of the intention of this series of posts is to illustrate how transparent these markets actually are and, consequently, how much more powerful and fair they can be if more widely used by key national players.

Thin Liquidity Is Not a Policy Win

It is tempting to read numbers this small as a kind of safety: a market too shallow to matter is a market too shallow to threaten anything. We have a different view.

This is the reliability problem we opened with. A mid that can sit still for 17 days, an ask that is sometimes not there at all, and a pool that cannot absorb $10,000 are not the shape of an instrument people can depend on. Demand for liquid digital Naira exposure does not wait for the regulated venue to catch up. It routes to USDT P2P, where Bybit already hosts the deepest market for the Naira, and to informal OTC desks.

This does not mean the Central Bank of Nigeria should turn a blind eye to permissionless growth. The substitution risk is real, and it is what recent BIS and IMF literature warns about. The IMF's modelling adds a sharper point: capital flow measures can increase circumvention when the foreign-stablecoin channel remains open. Keeping the domestic market thin does not make that channel close. It makes the foreign one the default.

So the real policy question is not whether Nigerians will hold and trade digital dollars and Naira. They already do. The question is whether that liquidity develops inside a transparent domestic perimeter, or leaks into rails that are more difficult to observe.

Open Liquidity

The future of cNGN is not a choice between no liquidity and uncontrolled liquidity. We’re looking for the middle ground: enough depth and market making for users to trust the asset, with enough transparency and controls for the central bank to trust the market.

Part of that package already exists. cNGN has reserve backing, public attestations, and redemption standards: see cngn.co/transparency.

We open sourced simple-mm because it is the market layer. It is is where practitioners can meet regulators halfway:

- Market-maker reporting on inventory, spreads, venues, and abnormal conditions.

- Circuit breakers for abnormal premiums or discounts, rapid flow changes, or stale reference prices.

- Source-age disclosure for every displayed quote, so a 17-day-old mid can never masquerade as a live price.

None of this is hypothetical. Every number in this article comes from data and scripts in our open repo: the order book snapshots, the full onchain swap history, the stress episodes. A cNGN market made in this manner would give the CBN more visibility than it has into any informal channel. The same transparency that lets us find one lonely ladder healing the spread is available to a supervisor, in real time, at essentially no cost.

That is also why market making in a market like this is monetary infrastructure rather than just trading. Good market making is not only tighter spreads. It is a discipline for saying which prices are fresh, which venues are executable, where inventory actually sits, and when to stop quoting. In a market where the deepest book can go 17 days without moving and the most active venue cannot absorb $10,000, no single venue can be trusted as the truth. The discipline of checking them against each other is the product.

Summing Up

The gap between "cNGN exists" and "cNGN is infrastructure" is not regulatory and it is not technical. It is this: 87 unique prices in 86 days, one ladder healing the spread, and hours at a time where one side of the book is empty.

Closing that gap is mechanical work. More participants quoting, more flow forcing the mid to update, more venues checking each other. Every number in this article comes from data and scripts in our open repo, so you can reproduce them, extend them to another pair, or prove us wrong.

If the first article was the argument for making these markets, this one is the baseline. When the numbers above look embarrassing in a year, the plan worked.

Notes

- Our Quidax data is not continuous: 88 gaps longer than five minutes, about 85 hours of missing coverage in total. Mostly infrastructure restarts on our side.